Mind the Gap

How disastrous would relegation be for two London rivals?

It is now undeniable. West Ham United and Tottenham Hotspur are in a relegation fight and probably against each other. Their two homes are six miles apart door to door and both hold 62,000 fans. But in many ways the similarities end there.

One club has spent the last decade building the most commercially ambitious stadium in English football, carrying nearly £1 billion of debt to do it. The other pays a peppercorn rent for a stadium it does not own and couldn’t afford to buy. One now has revenues (or rather the opportunity to generate in a Champions League season) over £600 million a season; the other generates less than half although both made it to the Deloitte Money League Top 20 for 2024/25. West Ham had the 16th highest wage bill in the World in 24/25 and Spurs spent more than Atletico, Inter, AC Milan, Juventus and Borussia Dortmund.

These are the sort of clubs that were meant to be too good (and too big) to go down in a post Super League world.

So, how serious is relegation these days for these clubs?

West Ham: trending down to going down?

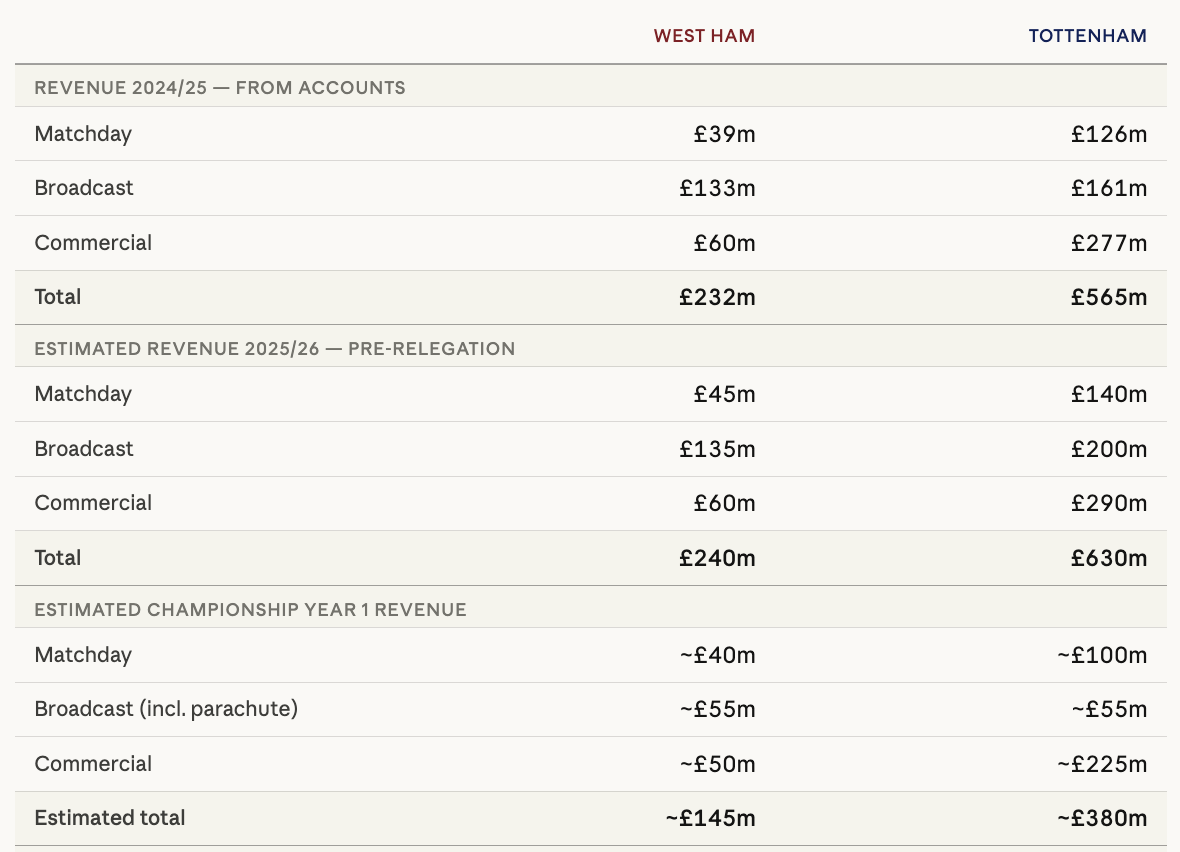

In the context of relegation risk, West Ham’s 2024/25 accounts make for uncomfortable reading. Revenue fell from a club record £270 million to £230 million as UEFA competition disappeared and the league finish worsened. Operating losses hit £105 million - the worst in the club’s history - driven by reduced player trading profits of just £20 million and a wage bill that has risen to another record of £175 million. Debt, which had been almost entirely eliminated by 2023, has climbed back to over £100 million following a £125 million facility with Rights and Media Funding Ltd (RMF) at interest rates likely in the order of 8-10% per annum.

So, whilst West Ham may not yet be relegated, the finances have already drifted into the “red zone”. The Going Concern statement states: “…under both the base case and severe but plausible case forecasts, mitigating actions are required in order to have sufficient liquidity for the Group to meet its liabilities over the going concern period.” In other words, even in the base case, West Ham still need to sell footballers.

The club attempted to reassure the reader of the accounts with this statement: “It is a feature of football clubs’ income streams that a significant element is known in advance because of its long-term contractual nature. Centrally negotiated broadcast and sponsorship deals are presently in place to at least the end of the 2027-28 season. The Group’s own major sponsorship and partnership agreements are also in place until the end of seasons 2025-26 and 2026-27 respectively. Season Ticket sales (including corporate sales) are made at the start of each season and represent the bulk of the Group’s match day revenue. Therefore, in the region of 75% of the Group’s annual turnover will be guaranteed, and in many cases received, by 31st July each year.”

However, this is only true in a Premier League year. West Ham have never played in the Championship in the cavernous London Stadium. The demand and timing of the purchase of season tickets and corporate hospitality are an unknown for a forthcoming season in the lower league. They have never tested whether you can sell 62,000 Championship seats nor at what price point. The central broadcast and sponsorship arrangements are indeed pre-sold. But relegated clubs receive around £75m less (at best) in the Championship even including the parachute payment in Year 1. So even if 75% of turnover may be known by the Summer (and there is a good chance it won’t be this time), it certainly does not mean it is 75% of West Ham’s recent historic income.

Relegated clubs have typically seen a 10-25% fall in Commercial revenue and more than a halving of Broadcast revenue. Most teams have maintained Matchday revenue but none of those teams have 62,000 seats to fill.

We can estimate that should West Ham finish 18th and be relegated, revenue will be around £240m for 2025/26 - Matchday £45m; Broadcast £135m; and Commercial £60m. Broadcast would fall to around £55m with a fire fight to maintain the other £100m. Likely total revenue would be £145m at best - a record for the Championship - but a challenge when set against the current cost base. The RMF loan obligations (probably £10m+ per annum in interest alone) do not pause for the Championship.

There are, however, some mitigating factors.

West Ham’s arrangement with the London Legacy Development Corporation for the London Stadium is unusual. They pay a token fee and that fee is understood to halve in the event of relegation. The wage bill would have to be restructured quickly and dramatically. At £180 million, it is approximately £140 million more than the Championship average. Relegation clauses in contracts will reduce that figure to some extent automatically and the club would look to move on players like Summerville, Mavropanos and Fernandes joining the Winter sale of Paqueta. What that means for the side if then promoted straight back to the Premier League is another matter.

Tottenham: snatching relegation from the jaws of a new era

When the Lewis family chased Daniel Levy out of N17 in September 2025, this was not the plan. The general idea was to loosen the purse strings. However, the relegation risk was underestimated in January and the club only bought and sold one first team player. On the face of it, none of the new regime’s decisions have worked.

They had inherited revenues of £565 million in 2024/25, the ninth highest in world football according to Deloitte’s Money League. That figure included £125 million in matchday revenue - higher than both Liverpool and Manchester City - and £275 million in commercial income, exceeded in England only by City, Liverpool and Manchester United. Ironically, the combination of Champions League football and the carefully managed vestiges of Levy on the wages and other costs side, will mean that whatever happens from here, Spurs will record an impressive set of financial results for the current 2025/26 season and accounting period with revenue topping £600 million for the first time.

But that revenue base is now at severe risk.

The broadcasting position is straightforward and mirrors West Ham. Tottenham would receive a year-one parachute payment of around £50 million and £5 million from the EFL, a drop of approximately £75 million. UEFA broadcast and prize money would drop another £70 million - the amount received for this season’s R16 Champions League exit. £200 million would become £55 million in the Championship.

The commercial position is more complex and in some ways more frightening. Spurs will have closed in on a total of £300 million for this season. Their shirt deal with AIA, worth approximately £40 million per year, is understood to contain relegation clauses and, anyway, it is up for replacement negotiations for 2027/28 during next season - AIA have already said they won’t be renewing.

Their Nike kit deal, worth around £40 million annually and running to 2033, would face pressure though likely a smaller absolute reduction given its long-term nature. The corporate hospitality business will struggle to sustain Premier League revenues for the 23 Championship home games that will include Lincoln City.

When Levy dreamed of the financial stability of hosting non-football events at the stadium it would certainly not have been about creating relegation-proof revenue streams. Yet here we are. The financial scale of up to 30 non football events is substantial and thankfully NFL fixtures, major concerts and boxing events are not contingent on Premier League status. That income stream estimated at tens of millions annually would persist through a Championship season and represents a meaningful structural advantage but it remains only mitigation. The commercial dip could be £50-75 million and even that assumes a strong season at the top of the Championship.

Despite having a similar capacity to West Ham, Spurs’ matchday revenue was around 3x that of West Ham in 2024/25 but probably nearer 4x this season (around £140 million). Whether Spurs could maintain anything over £100 million in the Championship would no doubt again depend on a winning and entertaining team and long domestic cup runs. In any scenario, the double whammy of no Premier League and no UEFA competition will be painful.

Alongside that revenue collapse would sit a massive debt pile. Tottenham now carry £850 million in financial debt, the highest in the Premier League, plus over £350 million in transfer debt - outstanding instalments owed to selling clubs for players already registered. Total debt of £1.2 billion, at interest payments that hit a club record of more than £30 million in 2024/25, does not obviously become more manageable when revenues fall by more than a quarter of a billion pounds in a single year. And there will likely be covenant breaches to deal with and associated costs.

Thankfully, Levy’s biggest achievement of his whole tenure was arguably one for the geeks. The long-term nature of most of the stadium financing with repayments stretching to 2051 at low fixed interest rates (typically less than 3.5%) means there is no short-term refinancing pressure.

The Telegraph has already reported that the wage bill (around £270 million for the current season) will fall significantly due to relegation clauses - it is no major surprise that Levy negotiated this but it is a very good job he did. This is the single most important factor in assessing the consequences of a Spurs relegation reducing costs by approximately £100 million compared to the current run rate. On top of this, for the benefit of both player and club, Spurs will no doubt sell a number of the biggest earners.

It isn’t a gap at all. It is an abyss

Both clubs face a version of the same nightmare, but Tottenham's is scarier in almost every dimension - more revenue to lose, more debt to service, more commercial contraction. West Ham's relegation would be painful and operationally chaotic. Spurs' relegation would be historically unprecedented - the largest single-year revenue collapse any English club has ever faced. The mitigating factors from relegation wage clauses to non-football stadium income to parachute payments matter but they do not come close to plugging the gap.

Six miles apart, two clubs, one abyss. The football will decide and the finance guys will deal with the consequences.

Nice article Stefan and of course we are approaching a defining moment for Tottenham. It’s odd don’t you think that since the inception of Deloitte’s Richest 20 Football Clubs in the World, report in 1998, Spurs have appeared on this list 25 times! As of the end of 2025 they are listed as the 9th richest club in world football. But here’s the rub; the financial model that has made them so rich off the pitch is also responsible for making them bankrupt on it. Now on their 30th manager since 1992 nothing will change beyond the ridiculous statements about ambition. De Zerbi, IF he keeps the club in the PL, will face the same unachievable instructions as the previous 29, compete with the super clubs whose reserve left back earns more than your fucking first choice striker!!!😀⚽️